Menu

What Is an Exchange?

- An exchange is a centralised marketplace for trading financial assets.

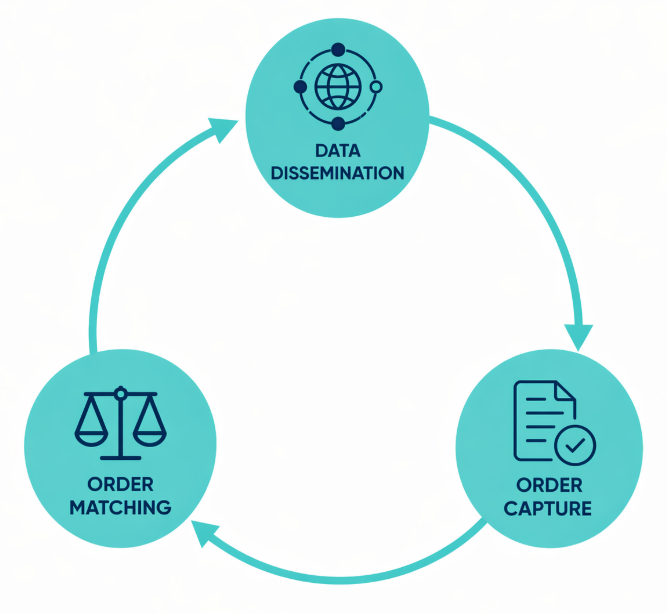

- Exchanges perform three important interlinking roles: data dissemination, order capture and order matching.

- When most people think of exchanges they think of stocks and shares but there is a wider world too.

Exchanges are organised marketplaces that facilitate the buying and selling of financial instruments. An exchange can be understood on two levels: as an economic institution that enables financing and as a technical system that performs specific operational functions. Separating these two perspectives helps clarify what exchanges are, how they create value and why their design and regulation matter.

Exchanges as economic institutions serve as vital components of both national and international financial systems by providing structured environments for trading, investing and capital raising therefore supporting the real economy and wealth creation.

- For traders, exchanges make it possible to buy and sell assets efficiently and at transparent prices.

- For investors, they offer access to liquid markets that allow capital to be allocated over time and portfolios to be adjusted as information changes.

- For companies and governments, exchanges support capital raising by facilitating primary issuance and creating secondary markets that give investors’ confidence they can later exit their positions which makes capital raising viable in the first place.

Modern economies rely on this infrastructure to channel savings into productive enterprises, establish credible prices and manage financial risk in a disciplined and transparent manner.

What Roles Do Exchanges Play?

As technical systems, exchanges perform three key interlinking roles: data dissemination, order capture and order matching. Data dissemination involves sharing information about quotes and trades, both before and after they occur, with market participants. This function is vital as it reduces information asymmetries, allows investors to make informed decisions and is essential for efficient price discovery. Once a broker routes orders, the exchange prioritises them so they can be matched transparently against opposite side orders (buy or sell). When matched, orders get executed contributing to price formation and turning into trades. The exchange is integrated into a broader ecosystem of systems responsible for clearing and settling the trade which together can be called market infrastructure.

Why Is Transparency Important for an Exchange?

Transparency is a core tenet of exchanges and well-functioning financial markets. For an exchange, transparency is multi-dimensional. It includes transparency of rules and processes, whereby order types, matching logic and market mechanics are published in advance so participants understand how the market operates. It includes price and market‑data transparency, through the dissemination of bids, offers, trades and volumes that support price discovery and execution benchmarking. It includes transparency of price formation, making visible how individual orders interact within a centralised mechanism to produce prices. It includes issuer transparency, via initial and ongoing disclosure requirements that give investors access to comparable company information. Finally, it includes transparency of participation, which varies by market in balancing anonymity during trading with traceability for regulatory and supervisory purposes. This multi-dimensional transparency fosters trust in exchange-led markets.

What Can You Trade on an Exchange?

Stock Exchanges facilitate the buying and selling of stocks or shares (of ownership in companies). Companies apply to list their stocks on an exchange in order to raise capital or funds for growth and operations in the primary market. The company will need to meet specific eligibility criteria, such as financial performance or governance standards, to protect investors and ensure market integrity. These requirements will often come from a regulator. Requirements from the exchange side revolve mostly around size and distribution of the offering. If they do, the company will be able to list through an Initial Public Offering (IPO). The subsequent trading of these shares happens in the secondary market.

Investors purchase stocks hoping for monetary gain. This can come in the form of dividend income or capital appreciation of the stock itself. These investments help investors to build wealth or save for longer-term goals such as retirement. It is well understood that stocks represent a powerful (if not the most powerful) way of investing for the longer term in the face of inflation.

Many exchanges also have a fixed income segment or market. These facilitate the buying and selling of fixed income-securities such as bonds and other debt instruments.

Similarly to stock exchanges, companies can apply to list their bonds on an exchange. The exchange reviews the issuer's application to ensure compliance with eligibility criteria and, once approved, the bonds are listed and made available for trading. Investors tend to purchase bonds when looking for a steady income over time, though capital appreciation may play a role too. They typically form part of a balanced portfolio of investments. Exchanges may also offer, or be focused on, derivatives contracts, such as futures and options. Derivatives contracts, as the name suggests, derive their value from an underlying asset such as stocks, bonds, commodities, currencies or indices.

Derivatives exchanges are primarily used by investors seeking to mitigate risk. Derivatives exchanges with a strong commodities offering are designed to transfer physical price risk, with contracts closely tied to real‑world supply, storage, delivery and consumption of tangible goods such as energy, metals and agriculture. By contrast, exchanges focused on financial derivatives primarily transfer financial and macroeconomic risk, using mostly cash‑settled contracts linked to indices, interest rates, FX, or volatility and serving investors rather than commercial hedgers. For example, a farmer can use futures to lock in a price for their crop, protecting against price drops. Derivatives contracts can either be physically settled (the actual asset is delivered) or cash-settled (the difference between the contract price and market price is paid).

In the past 25 years, exchanges have also increasingly offered ETFs, exchange‑traded funds that trade intraday like shares, while typically holding a diversified basket of underlying assets. They offer low‑cost, transparent and easily accessible exposure to equities, bonds, commodities and thematic strategies, allowing investors to gain broad market exposure, manage risk or implement tactical views without needing to trade individual securities directly. Many exchanges perform all of these roles, facilitating the trading of stocks, bonds and derivatives. Production and dissemination of market data related to these instruments is best considered as a joint product to order execution. A joint product is a good or service that is produced simultaneously with another product from the same process and cannot be created independently without also producing the other. This is similar to crude oil refining, where the same process simultaneously produces gasoline and diesel. Exchanges also facilitate the trading of a wide range of financial instruments, including government bonds, providing investors with access to diversified investment vehicles and sovereign debt markets.

Value to the Economy, Companies and Users

Different types of exchanges offer trading in different instruments or various types of instruments but they all share a common purpose – to facilitate the real economy by mobilising savings, allocating capital efficiently and providing transparent price signals. In the next piece we go into more depth on the value that exchanges bring to the economy, market participants and users.